{kind=link}

United States of America, Petitioner v William M Butler, Et Al...

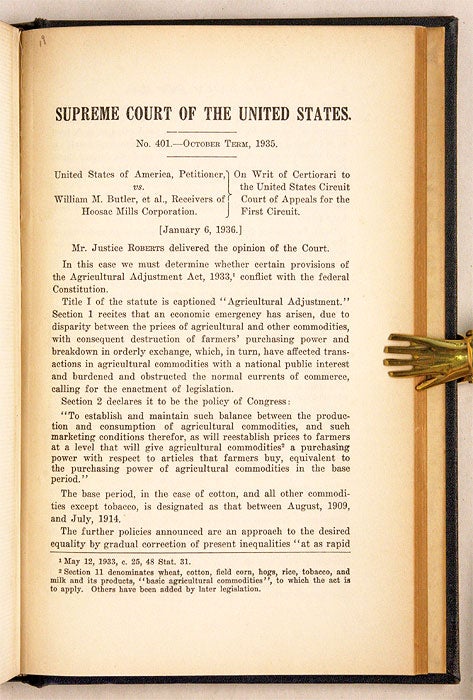

Documentary Record of Owens v. Butler, A Supreme Court Case that Invalidated an Important New Deal Program [Trial]. [Supreme Court, United States]. United States of America, Petitioner V. William M Butler, Et Al. Receivers of Hoosac Mills Corp., Rickert Rice Mills, Inc., Petitioner V. Rufus W. Fontenot, Individually and as Acting United States Collector of Internal Revenue for the District of Louisiana. Record. Briefs. Oral Argument of George Wharton Pepper. Opinions [spine title]. Washington, DC, 1935-1936. 19 items, various paginations. Folding tables. Pamphlets in wrappers bound in cloth, gilt title to spine, bound-in typewritten table of contents. Some rubbing to extremities with minor wear to corners, faint vertical crease through spine. Minor edgewear and a few tears to folding tables, internally clean. $1,500. * Assembled by an unknown attorney or law clerk, the 19 items in this volume, a 2-part transcript, 15 briefs, an oral argument and the opinion of U.S. Supreme Court Justice Owen J. Roberts form a documentary record of Owens v. Butler [297 U.S. 1 (1936)] the case that brought about the demise of the Agricultural Adjustment Act of 1933. Part of Roosevelt's New Deal, this was a Federal law that aimed to raise the value of crops by paying farmers and ranchers to reduce production. The money for these subsidies was generated through an exclusive tax on companies that processed farm products. This led to a series of seven suits by processors, who believed they were being taxed unfairly. The most important of these was Owens v. Butler. As framed by the plaintiff's lawyers, it asserted the right of a taxpayer to question the validity of a Federal tax. The Court decided in favor of Owens, ruling that the taxes instituted under the 1933 Agricultural Adjustment Act were unconstitutional under the Tenth Amendment. As argued by Justice Roberts, the tax was not valid because it was established in conjunction with coercive contracts with proceeds earmarked for the benefit of farmers complying with the prescribed conditions. The court also held that the basic premise of the act, paying a farmer to produce less to manipulate prices, went beyond the powers of the national government. The issues raised by Owens v. Butler were addressed by the Agricultural Adjustment Act of 1938, which continued the.

Price: $1,500.00

Book number 66002